Australia’s jobless figure fell by 0.1 percentage points in February after a shock rise in January.

The rate of unemployment fell to 6.3 per cent in February, down from 6.4 per cent in January, spelling some positive news for Australia’s floundering economy.

There are now 777,300 unemployed jobseekers in Australia, a decrease of 15,800, according to the Australian Bureau of Statistics.

The number of employed people, meanwhile, now stands at 11,652,400 an increase of 15,600.

The ABS said the increase in employment was driven byincreases in both full-time (up 10,300) and part-time employment (up 5,300). The employment rate increased for both men and women.

The figures also revealed that the labour force participation rate decreased to 64.6 per cent in February 2015, from 64.7 per cent in January 2015.

The collective number of hours worked in February went up by 13 million hours to 1,620.8 million hours, a 0.8 per cent increase.

The ‘grey army’ is a key to Australia’s future prosperity, according to Treasurer Joe Hockey. But what can the government do to increase participation of older people in the workforce? Its Restart program which offers employers $10,000 to hire an unemployed older person for two years has been a flop so far. Since last July, 956 people have benefited, the Employment Minister, Eric Abetz’s office told me. The program was expected to help up to 32,000 a year. Another program called Corporate Champions, aimed mainly at helping firms retain older workers, looks destined for the chop despite support in the business community. Corporate Champions was a Labor government initiative that was supposed to run for three years from 2013-2016. It’s proven so popular the allocated money has run out after a year, and no new companies can sign up.

Despite a surge in mature-age employment in the past 15 years, Australia has one of thelowest workforce participation rates for older people in the developed world. A higher proportion of older people is in work in New Zealand, the U.K, Sweden, Canada and the US. It’s relatively unusual to see someone of pension age strap-hanging on the bus in the morning peak hour. Can this be changed?

I think there’s no doubt Australia’s workplaces should harness the experience and wisdom of older people, and their contribution to the GDP. A lot of Australians can’t wait to retire; others want to work till they drop. A third group is in-between – they’d stay longer at work if more flexible work conditions were on offer. “Mature workers want to work longer but differently,” Alison Monroe, of Sageco, an employment consultancy, told me.

Many in this in-between group retire as soon as they can access their superannuation or the pension, or if other needs or desires pull them away. Because they want to pick up their grandkids from school a couple of days a week, or play golf on Fridays, they exit the workforce without exploring options. They assume bosses will be pleased to be rid of them.

That’s what Cynthia Cato 63 assumed when she resigned. She was in the young people’s business of advertising. She loved her job as a proof reader at the advertising agency. But she’d lost the affordable rented accommodation she’d enjoyed in Sydney for 30 years after the owner died. As a single woman, she couldn’t afford to buy near the city. But she could afford to buy in the countryside. She bought a beautiful cottage in rural Victoria, and she hoped she’d get a job packing shelves in a supermarket. “The managing director of the agency asked to see me. He said, ‘Cyndi, I’m not in the habit of letting good people go’ and so they worked out a deal,” Cynthia told me.

Cynthia now works from her rural Victorian home for the Sydney-based ad agency and couldn’t be happier. “If you have the internet, there’s no reason you can’t make a contribution to the workplace,” she said. “Older workers are prepared to give 110 per cent. We’re willing and reliable.”

The Corporate Champions program is geared mainly at this particular group – the workers who given flexibility could be persuaded to stay longer. Holding on to the existing mature-age workforce is where the big potential lies to increase participation. When the National Australia bank, one of the Corporate Champions, surveyed its mature-age workforce it found 91 per cent said they would work longer if they could work more flexibly; 62 per cent of staff leaders as a result of the program took steps to reduce barriers for older workers.

The Corporate Champions program has involved 486 big and small companies. Government funds don’t go to the companies but to approved providers who survey staff on retirement intentions, what it would take for them to work longer, and so on. Transition-to- retirement seminars in company time for workers have shocked some into knowledge of their true retirement financial position. The program appears to have been useful in educating both employees and employers. But last week’s Intergenerational Report mentioned only Restart as a government initiative for mature-age workers, signalling the possible end of Corporate Champions.

So many programs in this mature-age workers’ space have come and gone, from the “Wise Workforce” program of the Howard government to Labor’s Jobs Bonus. Many are not well thought-out or given a chance. Restart needs a bit of time to show it’s not a complete waste of money. And Corporate Champions should not be ditched just because it was a Labor initiative if it’s shown to change attitudes and practices.

More direct ways to keep older workers at the grindstone also need consideration. The most obvious is to raise the age at which superannuation can be accessed to the pension age. What’s your view of that? By 2023, the pension eligibility age will be 67 but access to super will be at age 60 (from 2024). Maintaining the gap provides a lure to the better-off to retire. Most importantly we need an economy that creates enough jobs for young and old. As for unemployed older people who are desperate to re-join a grey army of workers, they need a better deal. Higher penalties for age discrimination, and more naming and shaming of errant firms are needed to jolt employers and recruitment firms into changing their ways. The nicely, nicely approach hasn’t worked.

Assistant Employment Luke Hartsuyker says local employers need to start seeing the value of older workers.

The Federal Government’s Intergenerational Report, released yesterday, found people will need to retire much later in decades ahead due to the ageing population.

Just 13 percent of people aged over 65 are currently working or looking for work.

Older workers bring to their enterprise a wealth of experience

Assistant Employment Minister and Cowper MP, Luke Hartsuyker

Mr Hartsuyker said those numbers are going to have to rise, as people continue to live much longer lives.

The Cowper MP said employers also have a role to play, in placing more trust in older workers.

“I think it’s important that employers actively look for the benefits that older workers can bring,” he said.

“The Government has a role to play in providing incentives, where appropriate – that’s an important step.

“But I think its important that employers take into account that older workers bring to their enterprise a wealth of experience, a lifetime of experience.”

Mr Hartsuyker said the future of the nation’s economy depends on people working much later into their lives.

“That’s an important element, that we engage our older workers in the workforce, keep them in the workforce and keep them contributing, if we’re going to have the sort standard of living that we want for our future.”

Australia’s prosperity is at risk of being put under increasing pressure over the next four decades unless Australians work longer and productivity is improved, according to a major report due to be released today.

The ABC understands the Intergenerational Report, looking at population and budget projections to 2055, also states that economic reform is “crucial” to improve living standards. The document will be released by Federal Treasurer Joe Hockey today. Like previous long-term forecasts, the report will predict that the proportion of working Australians will decline as the nation’s population ages. By 2054-2055, the workforce participation rate is expected to be 2.2 per cent lower than today at 62.4 per cent. While the report will state “it is fantastic Australians are living longer, healthier lives” it warns there is a risk to GDP and income growth unless the Government can grapple with these demographic changes. It will suggest those not in the workforce, in particular older Australians and women, need to be encouraged to get a employment, re-enter the workforce, or prolong their careers.

To do that, the report will advocate policies to improve the accessibility of childcare, more flexible working conditions and the removal of discrimination. Australia currently trails Canada and New Zealand in terms of total workplace participation, though gains have been made in recent decades. For example, the report will show the number of working Australians aged 55 to 64 increased by roughly 18 per cent between 1978-1979 and 2013-2014. Also, the number of women in work has increased by 20 per cent since 1974-1975.

The Government is likely to use the Intergenerational Report to make the case for politically difficult policy changes in the next budget. The document will say reforms “to improve productivity will be crucial to achieve the growth in living standards” and wages. It will show average income levels have risen from about $40,500 in the early 1990s to about $66,400 today. “For every hour that is worked, Australians today produce twice as many goods and services per hour of work than they did in the early 1970s … It is no coincidence average incomes have almost doubled,” the report is expected to say. Assistant Treasurer Josh Frydenberg said the “landmark report” was a vital addition to complex national policy debates. “The detail it describes … will help the public understand the context for the Government’s economic decision making over the years ahead,” Mr Frydenberg said.

Labor and Greens wary of politicisation

The Intergenerational Report will also point out that the Government needs to ensure spending is sustainable. It will contain three forecasts of the nation’s cash deficit in 2054-2055. Under the policies of the Labor Government, the report suggests the cash deficit would be 12 per cent of GDP. But under the policies the Abbott Government has managed to pass so far, it forecasts a deficit of half that, or roughly $266.7 billion in today’s dollars.

This should be an independent report and I am worried it will be used to justify savage cuts in the budget.

Greens Senator Richard Di Natale

Also, under the policies the Abbott Government has proposed but not passed, it forecasts a surplus from 2019-2020. The Opposition says it is wary the Government is manipulating the report to try to justify its “unfair budget”. “This Treasurer has manipulated the timing of the release, he’s manipulating the content,” Shadow Treasurer Chris Bowen said. “We know that he hasn’t accepted the Department of Immigration’s advice about what the population figures in the report should be and he’s now bringing down a chapter on the Labor Party, it appears.” The Greens plan to refer the report to a Senate committee, to scrutinise its underlying assumptions and forecasts. “So far the discussion we are hearing around the Intergenerational Report seems to indicate we’ve arrived at a conclusion before we’ve even looked at the issue in detail,” Greens Senator Richard Di Natale said. “This should be an independent report and I am worried it will be used to justify savage cuts in the budget,” he said. Source: abc.net.au

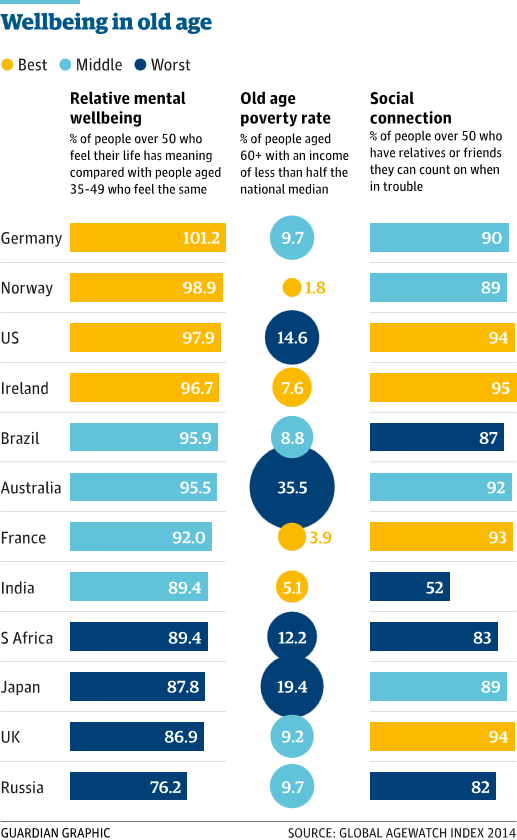

Australia’s notoriously labyrinthine $150bn (£75.8bn) welfare system last week underwent a major review, which essentially recommended an overhaul. However the Commonwealth-funded age pension was conspicuously absent. A politically sensitive topic, it was not in the scope set by the conservative Abbott government, despite it being the largest and most expensive part of Australia’s social security.Australians are living and working for longer. By 2013 the number of Australians aged 65 and over had increased by 533,000 from five years previously, and 17% of people aged 45 and older expected to work beyond the age of 70. In 2012-13, more than half of all retired men and a quarter of retired women named the government pension/allowance as their main source of income, a 45% increase on the number who told the Australian Bureau of Statistics they relied on it when they first retired. Superannuation payments (9.5% of a salary contributed by an employer) have been compulsory since 1992.State pensions are available to Australian residents over the age of 65 (67 by 2023) who have lived in Australia for at least 10 years (with some exceptions such as refugee status) and who meet income and asset requirements. In 2011, that translated to 60% of Australians of qualifying age. People who work past the pension age can still receive partial benefits or a lump sum under incentive schemes.Each fortnight pension recipients get a maximum payment of A$776.70 (£392) for singles, or A$585.50 (£296) if you are part of a couple. A payment supplement of up to A$63.50 (£32.13) a fortnight covers a pharmaceutical allowance, on top of Australia’s publicly funded universal healthcare benefit scheme, and utilities allowances. Each state and territory also offers cheaper travel and retail discounts to people over 60. Additional services, which are means-tested and partly financed by contributions from a recipient’s pension after a departmental assessment of what is needed, include the Home Care package, and the Home and Community Care package. People over the age of 65 can apply, or from 50 if they are Aboriginal or an Torres Strait Islander. Helen Davidson, Darwin

Germany

At the core of the German welfare benefits system is the comprehensive social insurance system into which most workers pay, which includes healthcare provision, unemployment insurance and pension insurance. Once you pay into all these parts of the system, (about 15.5% of your salary for healthcare, 3% for employment insurance, nursing care insurance, 2.2% or 1.95% for those with no children, 18.9% for pension insurance – most of these shared with an employer) you are entitled to a range of benefits, including healthcare for older people. Prescriptions and glasses are covered by that system so don’t have to be applied for separately, and are not classed as benefits.

A person continues to pay into the health insurance system once they are drawing a pension, unless they don’t have the means. Roughly speaking, on retirement, individuals receive half to two-thirds of net income as a pension. About 85% of the workforce is enrolled in the system. There is no legally set minimum or maximum pension.

The normal retirement age for everyone born after 1964 is 67 years. Women who take time off to have children have their contributions topped up by the state. But an OECD report published this week shows that Germany has the widest pension benefits gap between men and women in Europe and the US. The average monthly pension received is around €1,052 (£767.46) for men in the old West German states, and €1,006 (£733.9) for those in the old East German states, while for women the figures are €521 (£380) and €705 (£514). Kate Connolly, Berlin

Japan

Roughly one in four Japanese are 65 or over – that proportion is expected to rise to one in three by 2025. Pride that life expectancies for Japanese men and women are among the highest in the world is tempered by concern over how to pay for welfare in the coming decades, when there will be fewer people of working age to foot the bill. In 2012, the full basic pension was ¥786,500 (£4,342) a year, 16% of average earnings of 4.79 million yen (£26,443) a year, according to OECD figures. Everyone aged between 20 and 59 is expected to enrol in the basic national pension scheme, but only those who have paid in for a minimum of 25 years are eligible to draw a pension when they retire at 65. Full-time company employees and their spouses are automatically included in the employees’ pension scheme, which provides additional contributions to the basic state pension, proportional to an individual’s salary. The government estimates that about 85% of Japan’s workforce draw from the employees’ pension scheme. The fuel allowances for low-income residents will be cut by about ¥3bn (£16.2m) in this financial year. People aged 75 or older only need to shoulder 10% of their medical costs unless they have a high income. Everyone else pays 30% of the total cost. Some cities offer reasonably priced annual passes that enable elderly passengers unlimited travel for a year. Justin McCurry and Chie Matsumoto, Tokyo

Nordic countries

Unlike Sweden and Finland, in Norway pensions are holding up, and poverty among pensioners is actually falling dramatically, despite rising average wages. The official pension age has been 67 for both men and women since the 1970s, but it is possible to draw a full old-age pension from 62 and continue to work full time, while there is a range of options to draw a partial pension. But 67 remains the age when most people aim to retire – and the age at which people on disability benefits are transfered to pensions. Norwegians can continue to accrue pension entitlement until they are 75. Norway’s pension system is in transition, and currently two versions are in operation as the old one is phased out. The outgoing one is a defined benefit scheme comprised of a flat-rate universal benefit, an earnings-related second tier and a minimum benefit floor of almost 50% of average earnings after tax. It is a strongly progressive, egalitarian system due to the comparatively generous level of minimum protection and a decreasing replacement rate for earnings above the average annual wage. Marginal tax rates on pension income rise rapidly. A worker in Norway with 40 years’ contributions on an average wage can expect to enjoy a pension of about 67% of their previous income after tax. A new system is gradually taking over that consists of a defined contribution scheme, plus a minimum guaranteed pension. The payouts from this scheme are subject to a life expectancy adjustment, implying that old-age benefits for each new cohort of pensioners will be reduced in proportion to increases in longevity compared to 2010. Employment among older people is high in Norway, with more than 70% of people aged between 55 and 64 still working – well above the EU average of around 50%. In Sweden, pensions used to be more generous than in Norway, but the average pension is now just above 50% of wages, and it is expected to dip below that level if life expectancy increases and the retirement age is not postponed. The guaranteed minimum pension is about one-third of the net average wage. Pensioners in Sweden and Norway get discounts on public transport, entry to museums and an income-tested housing allowance is available. Pensioners – like other people in need – can also apply for social assistance to cover one-off payments and special needs. David Crouch, Gothenburg

Russia

The legal retirement age in Russia is early by European standards: 60 years for men and 55 for women. There has long been talk of raising the age, but given that male life expectancy is only just above 60, the move would be deeply unpopular. Russia’s finance minister said in a recent interview that the pension age should be increased gradually until it is 63 for both men and women. There is also talk of introducing an income test for pensioners – currently none exists and working pensioners or those receiving money from investments or other sources can still claim their pension. Workers involved in certain categories of hard labour, those who have spent more than 15 years working in Russia’s far north, and mothers of more than five children, are entitled to begin receiving their pensions earlier. A new points-based system is being phased in that will determine how much money pensioners receive based on how many years they worked. Currently, the basic state pension is around 4,000 (£40) roubles per month, but almost all pensioners receive a number of add-ons, and the average pension across the country is around 11,000 roubles (£110) per month, which is a little under one-third of the average salary. Some regions have particular allowances, for instance pensioners who have been registered living in Moscow for more than 10 years have their pensions topped up to at least 12,000 roubles by the Moscow city government.Pensioners also have a number of travel subsidies, discounted medicine, as well as small savings in certain supermarket chains, usually offered on particular days of the week. There is no guarantee of the security of Russia’s pension fund further down the line, and indeed it was recently admitted that 243bn roubles (£2.4bn) had been redirected from the pension fund to pay for costs associated with annexing Crimea. Shaun Walker, Moscow

United States

As the country ages there is no shortage of local, state, national and not-for-profit initiatives that cater to older citizens’ needs. From prevention of elder abuse to ageing awareness to help with nutrition, assistance programmes are a common feature in many communities. Take the “Campus Kitchens Project”, which along with the older persons’ organisation, AARP Foundation announced in 2014 a three-year renewal of its outreach effortsusing student volunteers to combat hunger and isolation among older people. With an estimated 9m older Americans at risk of hunger and the number of hungry people over 50 up by 80% in a decade the initiative harnesses a number of student-run kitchens at colleges across the country to help tackle food insecurity. Meanwhile in Pennsylvania, one project, “Coming of age”, under the auspices of a collection of organisations, including the state branch of AARP has trained administrators in methods to revamp “seniors centres” to make them more appealing for older people to spend time in with numerous benefits including reducing social isolation. While there are plenty of examples of inventive community-based initiatives, there are wider challenges not least of which is funding retirement. Exactly what income and benefits an individual receives when they reach 65 depends on a host of factors including which state they live in, whether they continue working past retirement age and in what capacity, the level of private or public sector employment-based pensions and other savings or investments. The Pension Rights Center in Washington DC and the Pension Policy Center report that of the 44.7 million Americans over the age of 65 in 2013, half had a total annual income of less than $20,380 (£13,271) – from all sources. Most US retirees receive income from social security, a federal social insurance programme to which people contribute via direct taxation. In the absence of a national state pension, it is the primary source of income for many and widely regarded as the foundation of retirement income. In 2013, 85% of older Americans received monthly social security benefits. The average annual benefit from social security for retired workers in 2013 was $15,132 (£9,852). According to the Social Security Administration, the national average wage in the same year was $44,888. For three out of five people over 65 who receive social security benefits it accounts for half of their total annual retirement income but it is particularly important for lower income Americans. In 2012 one in four people over the age of 65 received all of their income from social security. According to the Global Age Watch Index 2014 the modest nature of social security payments and the high reliance on it means that the US has a higher incidence of elder poverty than most other countries One of the most valued public services available to older Americans is Medicare, a national health insurance system with almost universal coverage. According to Global Age Watch the programme provides “good access” to medical services and preventative care. However wWhen it comes to access to services for older people with long-term care needs, however, there are many barriers to obtaining affordable, quality provision because most adults don’t have separate insurance coverage for these. Mary O’Hara, Los Angeles

South Africa

Old age pensions are provided to people above the age of 60 earning below R49,920 (£2,763) if single and R99,840 (£5,527) if married, and whose assets do not exceed R831,600 (£46,041) if single and R1.7 million if married. Beneficiaries must not be maintained or cared for in a state institution, and should not be in receipt of another social grant. An elderly person is typically eligible for a grant of 1,350 rand (£75) per month. Government guidelines state: “It should be noted that social grants for adults are paid on a sliding scale – the more income and applicant has, the less he/she will receive for the grant.” They can turn to extended families and NGOs for help. The services NGOs offer include social support groups, training and education, income generating projects, frail care services, transport to health facilities and luncheon clubs and home based care, according to the Older Person’s Forum. But most of these services are non-existent in rural areas. Nearly three million people were old age pension recipients in 2013/14. There are private companies that offer these benefits to pensioners – such as Specsavers with spectacles and some bus companies regarding travel.South Africa has one of the largest voluntary retirement funding systems in the world (and for the large proportions of people in employment, these arrangements are mandatory conditions of service). There are programmes of support in provincial social department for old age homes.There is broadly free healthcare in public health facilities. Public housing and transport also benefits many elderly people. Those retiring early have their pensions cut by 3.6% for each year, except those forced into early retirement, whose pensions can by cut by a maximum of 10.8%. David Smith, Johannesburg

Italy

The state pension is €219-€230 (£159-£167) per week for people under 80 and €240.30 (£175) for over-80s, depending on Older people, like all other Italians, receive free healthcare under the national health system. The services are either delivered free of charge, or patients pay for them and are reimbursed. Other benefits differ from region to region. For example, residents in Rome over the age of 70 are offered free bus and metro passes. Stephanie Kirchgaessner, Rome

France

The legal retirement age in France now stands at 62 for people born between 1955 and 1973. However a full state pension is only awarded for those who have worked 40-43 years. Those born after 1973 will have to work for 43 years to obtain a full pension at 62. In certain cases, including those who have taken time out for parenting or taking care of a disabled person, it is possible to claim a full pension at the age of 65 (or 67 depending on the date of birth) regardless of how long the individual has worked. For private sector workers, the full pension takes into account the 25 best years worked, with an allowance for inflation, and can total half their monthly salary. Civil servants have a more generous scheme: they can retire on a state pension of 75% of average income, calculated on the basis of their last six months in work (minus bonuses). However under reforms announced last year, civil servants will have to work an extra two years – 43 instead of 41.5 – to receive a full pension, bringing them into line with the work period requirements of the private sector, even though the calculation remains different. For unemployed pensioners, a single person with less than €9,600 (£6,988) per year or a couple with less than €14,904 per year can claim an allowance called the allocation de solidarité aux personnes agés (Aspa), or elderly persons solidarity benefit. In the case of a single person surviving on €7,000 a year, the Aspa allowance would be €2,600 (£1,893) – calculated according to the €9,600 benchmark figure minus the €7,000. A couple with €13,000 would receive €1,904 per year. Anne Penketh, Paris

Ireland

The state pension is €219-€230 (£159-£167) per week for under-80s and €240.30 (£175) for over-80s, depending on social insurance contributions while working, regardless of any income from private or occupational pensions. Pensioners, like those in receipt of long-term social welfare payments or those who can prove they cannot provide their heating needs during winter, are entitled to a means-tested weekly winter fuel allowance of €20 (£ 14.54) per household. Those over 70 receive a free TV licence and in some cases are eligible for means-tested free electricity and gas depending on their fiscal circumstances. All pensioners receive free bus and rail travel, not only in the Irish Republic but across the border in Northern Ireland. Henry McDonald, Dublin Source: The Guardian

To safeguard our way of life, we must keep people in jobs and the economy growing.

Older workers have expertise based on years of experience and make an important contribution to the economy. Photo: James Alcock

I suspect if you were to ask many of those in their late 40s and older if ageism could hold Australia back, their answer would be “yes”. That disappointing view would invariably be based on their personal experiences in the workforce.

Ageism will hold us back because, with an ageing population, we need to increase participation by older workers in the workforce.The evidence over recent decades indicates older people are underemployed for longer periods than younger workers. Australian Bureau of Statistics figures show more than 35 per cent of jobseekers aged 55 and over stopped looking for work because they believed potential employers thought they were too old.

As a society, we are discarding valuable older workers far too early.

These older people excluded from the workforce account for more than half the total number of jobseekers who gave up looking for work.

Older workers face ageist stereotypes and biases, especially in the workplace and in recruitment. These negative attitudes label them as too costly, too inflexible and too difficult to train. As a society, we are discarding valuable older workers far too early.

The stereotype of people studying in their youth, working hard in a career and retiring at 65 no longer applies. We need to change the way we view older people. This is not just because it is demeaning and discriminatory, but because we need to revalue their potential contribution in the workplace.

To safeguard our way of life, we must maintain our incomes and keep people in jobs. In short, we need to keep the economy growing. One of the key drivers of long-term growth is widely recognised as having more people in the workforce.

Unfortunately, if we do not adjust our approach, the long-term outlook for Australia is lower economic growth. Why? Because our population and our economy are changing and that will impact heavily on our workforce participation.

The government will soon launch the 2015 intergenerational report. The report is the most comprehensive examination of demography and current policy. It evaluates how these changes will affect the economy and government finances over the next 40 years.

It will show there will be fewer people of traditional working age as a proportion of the population in the years to come. Over the next decade, the working population is expected to increase by 12 per cent, while the population over 65 is expected to increase by 36 per cent. That is, the number of people aged over 65 will grow three times faster than the traditional working-age population.

The number of people in the traditional workforce supporting those who have left the workforce will nearly halve over the next 40 years.

On the one hand, this a problem, because as the population ages and more people leave the workforce, tax revenues will struggle to fund the same level of government services we enjoy today. On the other hand, this is an opportunity to encourage greater workforce participation, especially among underappreciated and underutilised older people.

We must not fall into the trap of viewing an ageing population as a burden. Older people will be critical to maintaining the economic growth that has underpinned the advances in our standards of living and quality of life.

According to the age discrimination commissioner: “As a society, we have been slow to recognise that millions of older Australians are locked out of the workforce by age discrimination. We are only now starting to understand what a terrible waste of human capital this situation represents; a loss to the national economy and to businesses large and small, and a loss to the individual who is pushed out of the workforce prematurely.”

Deloitte Access Economics estimates a 3 per cent increase in participation by the over 55s would generate a $33 billion annual boost to the national economy. A 5 per cent increase in participation, would see a $48 billion boost to the economy.

If Australia’s workforce participation rate for those aged over 65 increased to that of New Zealand over the next 10 years, this would result in a boost to Australia’s real gross domestic product of about $40 billion in 2024-25.

Older workers contribute knowledge and skills based on years of experience and expertise. We need older people working and contributing to our economic growth.

Also, people who work longer accrue more superannuation savings and are less reliant on the pension during retirement.

There is a strong correlation between workforce participation and health status. Continuing to work protects against physical ill-health and poor mental health. Data shows people staying in the workforce past retirement age tend to have better health compared with those not working.

Older workers also report the need for flexibility in their working hours or part-time arrangements so they can fit in caring responsibilities or manage sickness or disability.

The decline in participation rates of older workers only aggravates the problem of age dependency and rising social expenditures. Ignoring a pool of productive workers in the face of a falling participation rate will affect our economic growth.

If these trends continue, we as a society will be contributing to a decline in our standard of living. So let’s reverse the traditional attitudes, embrace a longer life and look for ways to redesign our lives so we can enjoy prosperity along the way.

More companies are recognizing the value of mature workers—and they’re starting to hire them.

Things are finally looking up for older workers.

The latest data show the unemployment rate for those over age 55 stands at just 4.1%, compared with 5.7% for the total population and a steep 18.8% for teens. The ranks of the long-term unemployed, which ballooned during the recession as mature workers lost their jobs, are coming down. Age-discrimination charges have fallen for six consecutive years. And now, as the job market lurches back to life, more companies are wooing the silver set with formal retraining programs.

This is not to say that older workers have it easy. Overall, the long-term unemployment rate remains stubbornly high—31.5%. And even though age-discrimination charges have declined they remain at peak pre-recession levels. Meanwhile, critics note that some corporate re-entry programs are not a great deal, paying little or no salary and distracting workers from seeking full-time gainful employment.

Still, the big picture is one of improving opportunity for workers past age 50. That’s welcome news for many reasons, not least is that those who lose their job past age 58 are at greater health risk and, on average, lose three years of life expectancy. Meanwhile, older workers are a bigger piece of the labor force. Two decades ago, less than a third of people age 55 and over were employed or looking for work. Today, the share is 40%, according to the St. Louis Federal Reserve.

AARP and others have long argued that older workers are reliable, flexible, experienced and possess valuable institutional knowledge. Increasingly, employers seem to want these traits.

This spring, the global bank Barclays will expand its apprenticeship program and begin looking at candidates past age 50. The bank will consider mature workers from unrelated fields, saying the only experience they need is practical experience. The bank says this is no PR stunt; it values older workers who have life experience and can better relate to customers seeking a mortgage or auto loan. With training, the bank believes they would make good, full-time, fairly compensated loan officers.

Already, Barclays has a team of tech-savvy older workers in place to help mature customers with online banking. The new apprenticeship program builds on this effort to capitalize on the life skills of experienced employees.

Others have tiptoed into this space. Goldman Sachs started a “returnship” in the throes of the recession. But the program is only a 10-week retraining exercise, with competitive pay, and highly selective. About 2% of applicants get accepted. It is not designed as a gateway to full-time employment at Goldman, though some older interns end up with job offers at the bank.

The nonprofit Encore.com offers mature workers a one-yearfellowship, typically in a professional capacity at another nonprofit, to help mature workers re-enter the job market. Again, this is a temporary arrangement and pays just $25,000.

But a growing number of organizations—the National Institutes of Health, Stanley Consultants, and Michelin North America, amongmany others—embrace a seasoned workforce and have programs designed to attract and keep workers past 50. Companies with internship programs for older workers include PwC, Regeneron, Harvard Business School, MetLife and McKinsey.

Was I the only person in Australia who congratulated Treasurer Joe Hockey on his observation that the first person to live to 150 might already be born?

Not only have medical scientists confirmed the comment, the shock value of contemplating our 150th birthdays should have had all economists, employers, business chiefs and mid-age individuals focusing seriously on how to extend the working life of most Australians. Moving towards a stage where 70 rather than 60 becomes the average retirement age is what our economy needs, and what older people themselves are often seeking.

Health experts constantly remind us that the working older person is healthier than the non-working older person, and happier. These realities should provide a constructive context for the appearance of the Intergenerational Report. The IGRs, and we are up to our fourth, set out the long-term budget implications of ever-rising numbers of individuals living for more years on the age pension and public health, over a period where the proportion of the working population younger than 65 is declining.

The expenditures as predicted are unsustainable, but they are not inevitable. Obvious and realistic policy change would pull the figures into better balance, into “sustainability”. The objective of changing the ratios by increasing the numbers of older workers should be in this conversation from the beginning.

With past IGRs, positive policy opportunities have been drowned by waves of negativity about the unadorned outlook figures. The last Intergenerational Report spoke only of the “risks” and “challenges” of our ageing population, and the dramatic reduction of the proportion of those of working age to support those older than 65. It highlighted the pressures on health spending in relation to the ageing population.

It implied and was widely interpreted as insisting that all those older than 65 are in need of substantial and growing public support. It set up a dichotomy between younger/older as good/bad. It implied that ageing only meant illness, decline and burdening the public purse. The economic potential of older people was ignored. This approach perpetuates unhelpful stereotypes of older people and obstructs the development of a policy approach where younger and older generations can work co-operatively.

Why are individuals leaving paid work at 60, or often earlier, rather than 70? Even if they are more likely to live to 100 instead of 150, four decades without earned income and the satisfaction of work is too many. Age discrimination in employment is a huge barrier preventing older Australians from continuing in the workforce. One in five unemployed people older than 45 report that their main difficulty in finding work is that they are considered too old by employers. We know that one in 10 business respondents have an age above which they will not recruit – the average age is 50 years.

We also know that helping older people participate would boost our economy. Deloitte Access Economics research shows that increasing the number of Australians older than 55 in paid employment by 5% would result in a $48 billion impact on the national economy.

This can happen. The percentage of the people aged 55-64 in the workforce in Australia is 61.5 per cent, and has remained stable since 2012. Compare this to New Zealand, where the percentage is 74.4 per cent. Since 2012 Australia has dropped from 11th to 13th place for workforce participation of older workers among Organisation for Economic Co-operation and Development countries.

The longer people work, the more superannuation they will have. The IGR is an opportunity to review the longer-term effects of the current application of tax benefits for super.

Like other “too hard basket” changes, this policy should be brought out of the basket and included in the discussion. Tax-favoured superannuation was originally introduced so that more people could achieve independence in retirement. What is the public policy purpose of continuing the provision of substantial tax benefits well beyond the point where individuals have achieved the means to support a high standard of living in retirement? Might not those tax benefits be better redirected to those whose retirement savings fall well below an adequate standard and who have only the age pension in prospect?

Providing age pension benefits to increasing numbers of individuals who possess well in excess of the means for a very comfortable retirement might not be best practice in targeting welfare dollars. Requiring high-net-worth individuals to make a larger contribution to the costs of their aged care could be in the interests of improved fairness and efficiency and improved quality of care.

I hope the Treasurer’s release of the IGR data will bring into focus some realistic and purposeful discussion around these policy directions.

I see this Intergenerational Report as an important opportunity to present what could happen if we stopped age discrimination and increased the participation of older workers. Rather than emphasising doom, gloom and negative stereotypes, I urge the Treasurer to show what would happen if we mitigated the worst-case scenario by leading the world in employment practices that embrace fairness and improved opportunity for older workers through flexibility, retraining, and intergenerational initiatives.

We all understand the population is ageing. Surely now we are ready to have a conversation about how to realise the economic and social potential this longevity represents.

We all understand the population is ageing, and while comments by treasurer Joe Hockey that the first person to live to 150 may have already been born attracted some derision, it should come as no surprise. What is less easy to understand is the curious paradox that, as the workforce ages, the age at which workers are being labelled by organisations and recruiters as “old” is getting younger.

The way that many organisations and those recruiting for organisations construct old age is very different to the way that the authors of the soon-to-be-released Intergenerational Report are likely to construct older age. Our research into the management of age in organisations has found overwhelmingly that employees over the age of 45 self-identify as older. Further, there is a general sense amongst organisational decision makers that if you haven’t “made it” by the age of 40 you aren’t going to “make it” at all.

Declaring that you must have made it by 40 not only ignores the huge potential of people in their 50s, 60s and 70s, but it also doesn’t account for the fact that many women and men are ready to hit their stride in their 50s. Relieved of the heavy lifting responsibilities of parenting, they are able to devote themselves to their careers and to their employers.

Some companies have managed to see this potential and are beginning to think creatively about what having an older workforce profile means and how they can leverage its opportunities for increased productivity and innovation.

The advent of the corporation in the early and mid-twentieth century created a prototypical career/life cycle in which youth meant education, adulthood meant work and old age meant retirement. This may have served bureaucratic corporations of the past because it provided order and calculability to those who passed through it.

However, it is an out-dated way of thinking for the modern corporation Much of the discourse in the lead-up to the release of the Intergenerational Report pits old against young. Older people are constructed as an economic burden and younger people as resentful and angry. Yet our research into intergenerational relations in organisations found high levels of respect between younger and older people.

In particular, we found that younger employees greatly respected the knowledge and resilience that their older co-workers brought to their work. As the workforce ages and people stay in work longer, there is a huge opportunity to capitalise on the diversity of ideas, customer segments and product markets that an intergenerational workforce can open up to an organisation. Our research with a global engineering firm showed that the most innovative divisions were the ones in which teams were configured to include a broad range of ages, from new graduates to experienced workers over the age of 65. Respondents reporting learning from one another, and the shared experience flowed both ways. In these teams, the notion of experience wasn’t limited to time served, nor was it seen to expire once people had reached a certain age.

Words do matter. The way that we talk about age in organisations affects both internal employee engagement and also recruitment strategies. Those older and younger than the magic age of 35 to 45 often receive an unintended but powerful message that they have less to contribute to the organisation, and report lower levels of workplace engagement as a result. The language organisations use in their general marketing and specifically in their recruitment can send unintended signals that those over 45 need not apply.

One organisation we worked with wanted to recruit people 45 and older but was having trouble attracting candidates. We could show them that the wording of their job advertisements, “join a vibrant team that works hard and plays hard” and “working space is fresh and funky” was unintentionally signalling that older candidates were not welcome. We encouraged them to highlight aspects of the job that are most important to older workers: recognition of skills, work and life experience; the culture and values of the organisation; and the opportunity to learn new things. This last one is important because it is perhaps the most pervasive yet blatantly false stereotype about ageing. We don’t stop wanting to learn new things as we age.

If the fourth Intergenerational Report is to have the impact that the government, policy makers and employees of all ages are hoping it will, then it is business that needs to take the lead in re-imagining careers, shifting to an age-inclusive culture and establishing the organisational structures whereby employees of all generations can work with, for and alongside one another. Our prosperity and productivity as a nation relies on it.

The trouble with the way the media report developments in the labour market from one month to the next is that we don’t get a sense of the major shifts that occur over time.

So today let’s take a much longer view, examining the trends over, say, the two decades from 1993 to 2013. We’ll do so with help from an article by Professors Roger Wilkins and Mark Wooden, of the Melbourne Institute, published in the latest issue of the Australian Economic Review.

Note that this period covers most of the continuous economic upswing since the severe recession of the early 1990s. So most of the trends are reasonably good. It’s true, however, that we were knocked off track briefly by the global financial crisis of 2008-09 and in more recent years have suffered a slow deterioration in unemployment as the economy makes heavy weather of the end of the mining investment boom.

But that’s getting ahead of the story. Actually, it’s such a long story that today I’ll limit it to the side that gets least attention from the media, changes in the supply of labour. It’s best measured by changes in the “participation rate” – the proportion of the population of working age who are participating in the labour market by making their labour available, either by having a job or actively seeking one.

Taken overall, the “part rate” increased pretty strongly until 2008, when it began falling back. But all of this overall increase is explained by the increased participation of women, particularly those of prime age, 25 to 54.

There’s been a long-term slow decline in the participation of men. It’s explained partly by young males staying longer in the education system but mainly by older workers retiring earlier – voluntarily or otherwise.

But here’s where the story gets complicated. The trend to earlier retirement turned around at about the turn of the century, with participation by both men and women aged 55 and over rising significantly.

Got that? Now try this. Although more people are retiring later, the part rate reached a peak in 2008, has fallen since then and is likely to continue falling for years yet. Why? Because of the ageing of the population.

The trick is that even if the part rate is now rising in older age groups, population ageing means that an ever-rising proportion of the labour force is in those older age groups, whose rates of participation will always be a lot lower than the rates for people of prime age.

To show the significance of this ageing effect, the authors calculate that if the age structure of the population in 2013 was the same as in 1993, the overall part rate would be 2.2 percentage points higher than it actually is.

However, we do have some scope to moderate this demography-driven decline in participation. Wilkins and Wooden note that the rates of participation for 55 to 64-year-olds are between 7 and 14 percentage points higher in New Zealand than they are in Oz. If the Kiwis can do it, what’s to stop us doing it?

The part rate covers the quantity of people willing to supply their labour, but there’s also the question of changes in the quality of the labour being supplied.

The past 20 years have seen a big improvement in the skills – education and training – of the labour force, with the proportion of university graduates more than doubling from 12 per cent to 28 per cent. The proportion with any post-secondary qualification rose from less than 46 per cent to more than 62 per cent.

By the way, it’s likely that the continuing rise in women’s participation is largely explained by the dramatic increase in females’ academic attainment. The higher men and women’s level of education, the greater the likelihood they’ll be in the labour force – exploiting the commercial value of their skills – and the less the likelihood of them being unemployed.

Of course, another part of the labour supply story is immigrant workers. Immigration has long been a major source of additional labour and today accounts for more than a fifth of the labour force. What’s changed is that throughout the last century most migrants came on permanent visas, whereas today most come on temporary visas.

In March last year there were almost 900,000 people on temporary visas with work rights, including more than 200,000 on “457 visas” for skilled people and about 370,000 on student visas. If all these people actually participated they’d amount to 7 per cent of the labour force, the authors estimate.

Separate to this were almost 650,000 people on the special visas for New Zealanders, some of whom will prove to be only temporary residents. (Don’t forget Aussies have reciprocal rights to work in Kiwiland.)

We now grant about 125,000 457 visas a year and about 100,000 student visas a year. This compares with about 130,000 old-style permanent visas a year to skilled immigrants, many of which are given to people already here on temporary visas.

The authors observe that the shift towards temporary migration has probably had a big effect on the labour market.

“The availability of a flexible skilled immigrant workforce that can respond to changes in labour demand relatively quickly is likely to have improved the operation of the labour market, especially from an employer perspective,” they say.

Oh. Yes. To me the main drawback is not so much that employers may not try hard enough to find local workers to fill jobs, or that the availability of this external supply may limit to some extent the rise in skilled wages, but that it reduces employers’ incentive go to the bother of training young workers.

Still, we mustn’t forget that, these days, the economy is run for the benefit of business, not the rest of us.

Ross Gittins is the economics editor.Twitter: @1RossGittins